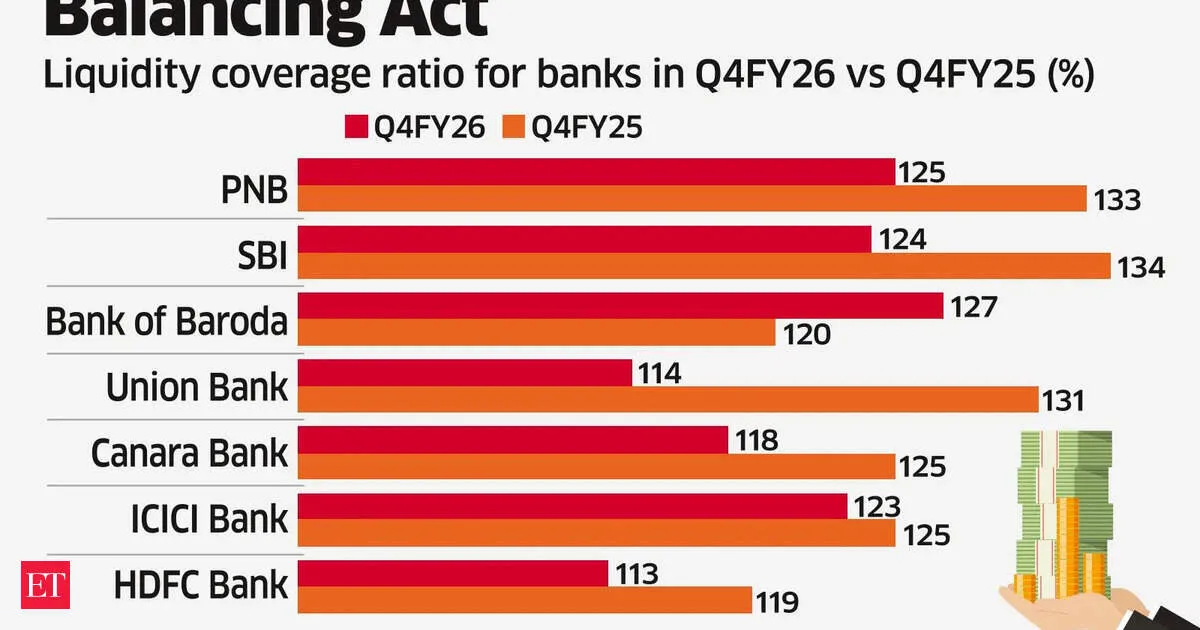

State-run banks in India are edging closer to regulatory minimums as liquidity coverage ratios fall, driven by loan growth outpacing retail deposit growth. In the March quarter, major PSU banks saw LCR drop by 10–12 percentage points to around 114%–118%, nearer the 100% threshold. Union Bank, Canara Bank and SBI reported sharp year-on-year declines while loans grew faster than deposits. Analysts warn the “easy” strategy of funding credit using excess liquidity is running out, though new norms from Q1 FY27 may ease runoff rates.

Small Finance Banks are increasingly leaning on secured products like gold loans to steady earnings and financial health, as unsecured microfinance continues to struggle with elevated bad-loan ratios. The shift aligns with regulator pressure to diversify away from concentrated risk. Larger banks are also expanding microfinance, but the overall pivot toward collateral-backed lending signals a strategy for long-term stability.

Your news, in seconds

Get the Beige app — every story in 60 words, updated hourly. Free on iOS & Android.

Sebi has moved to align India’s securitisation framework with RBI regulations for entities already governed by central bank rules. The proposal includes relaxing the 25% single borrower exposure cap, shifting disclosure duties to the servicer, and tweaking governance for SPDEs. The changes are aimed at enabling more single-asset deals while improving transparency across the process.

Sebi Chairman Tuhin Kanta Pandey said India’s banking and insurance regulators are not in favour of allowing lenders and insurers to trade in commodity markets, citing legitimate concerns. Separately, Sebi is preparing an advisory on emerging AI risks, warning that powerful models can exploit weaknesses at speed. The regulator is also set to roll out C-KYC 2.

The RBI has revoked Paytm Payments Bank’s licence under Section 22(4) of the Banking Regulation Act. The bank can’t carry out banking business anymore, but both the RBI and Paytm say it has enough liquidity to repay depositors. Refunds for savings accounts, wallets, FASTags, and NCMC cards will be handled through a court-monitored winding-up process.

The RBI has cancelled the banking licence of Paytm Payments Bank due to ongoing compliance issues. The bank can no longer accept deposits, but the Paytm app and core services are reported to remain unaffected. For users, this means you may still be able to use UPI and other payment features, even as the payments bank’s banking operations end.

Never miss a story

Set alerts for the topics and sources you care about. Download Beige for free.

The RBI has revoked Paytm Payments Bank’s licence, citing governance and management practices harmful to depositors and the public. The decision, under the Banking Regulation Act, takes effect from April 24, 2026 and will bar Paytm Payments Bank from operating as a bank. RBI will seek winding up through the High Court, while Paytm says it is not financially affected.

The RBI has cancelled the licence of Paytm Payments Bank, saying it can no longer conduct banking business under the Banking Regulation Act. The move raises fresh questions for customers and the wider Paytm ecosystem, as the regulator formally ends the bank’s authority to operate. Details on next steps for users are now the key focus.

RBI has cancelled the license of Paytm Payments Bank after previously barring it from accepting fresh deposits since 2024. The decision signals the bank can’t continue operations as it did earlier, putting its account holders and associated services in focus. The RBI action follows heightened regulatory scrutiny of payment banks and their compliance obligations.

Fifteen years after Basel III was meant to standardize bank capital rules globally, national regulators are applying it unevenly. The US, Europe and India are prioritizing local economic and political goals, creating different capital requirements across jurisdictions. The result is a less comparable international banking system where banks face shifting buffers rather than one common standard.

Reading on mobile?

Open Beige in the app for a smoother experience — free on iOS and Android.

HDFC Bank’s larger balance sheet could translate into bigger loan disbursals after the merger, while costs may fall due to recent regulatory streamlining. Updated reporting and delinquency provisioning rules for banks and non-bank finance companies are expected to reduce friction. HDFC’s focus on affordable housing and micro-lending can also help align its loan book with HDFC Bank’s development finance requirements.

Swipe through stories, personalise your feed, and save articles for later — all on the app.